For those wonderful, generous folks who’ve asked where they can leave me money, even after just a brief, “headline only” post such as this one (believe what you want, I’m NOT making this up, some people love me that much!), you can do so here. But, I don’t expect it. This one was not much effort.

Uncle Dreizin Wants YOU!

If you haven’t already, please sign up to my damn MAILING LIST! All this means, is that you’ll get my blog posts, in your email. I DO NOT mass-send anything but that. Please enter your email address, in the box below.

[email-subscribers-form id=”1″]

Donations

Please support my work, here.

COMMENTS POLICY

Comments and any associated weblinks or other references must be directly relevant, tangential, and responsive to specific facts or views within my own published material (not just to other comments), specifically the material above the given comments section that you are adding to. What this means, for example, is if I wrote about dogs and cats in the Ukraine, and only dogs and cats in the Ukraine, please don’t start babbling about life in Lugansk, or the horrible loss of life in general. THIS IS NOT A “DISCUSSION BOARD.” IT IS NOT A DEBATE PLATFORM TO DISCUSS IRRELEVANT HISTORICAL QUESTIONS, OR TO INJECT YOUR OWN PET SUBJECTS / INTERESTS, PHILOSOPHICAL MUSINGS, OR RANDOM RAMBLINGS THAT DON’T DIRECTLY, SUBSTANTIALLY BEAR ON WHAT I WROTE. Please, no disjointed / overcaffeinated rambling, which implies, among other things, no mentioning eight different topics in one comment, like a schizoid aiming to connect all the dots (if your mind is racing, take your Ritalin and calm the fuck down before you comment on this site); no “pet issues” or inquiries that have no direct bearing on what I wrote; no unclear/unexplained, irrelevant, or barely-relevant weblinks; no trying to write your own mini-blog news update digest in my comments; no batteries of questions like what about Donetsk and what about Kiev and what about the Big Offensive and how does this all end and where does blah blah blah (I will NOT respond to you, I will BLOCK you); no asking me what I think of some commentator whom I’ve never heard of; no Nazis; no Nazis pretending to be Jewish like “I’m a bar mitzvah boy, but I’m so ashamed of my people who are not the real Jews of Jesus’ time“; no “crypto” Jew-hating (when I have to read it three times before I’m sure it’s about Jews, then I permanently block your wise ass); no dogmatic Marxists; no using anti-Ukraine jargon or other “Nadsat” bullshit-speak that you picked up from The Saker, which no one outside of you and your freaky virtual friends can understand (e.g., Ukrops, 404, the vimiratis); no calling for the destruction or dissolution of the USA or its government; no calling for the destruction of Washington, DC; no calling for violence against current or former elected or appointed officials of the U.S. Government; no nonconstructive or hateful ranting about Jews (or Swej, Joos, Jooz, Jooze, Juice, Juize, Jewz, Jewze, J-Dogs, J-Dogz, J-Dawgz, J’s, Chews, Choos, Chooz, Chooze, Zionists, Zio-Nazis, Anglo-American Zionists, Amerizionists, Zionist Occupation Government, ZOG, IsraHell, Bibi SatanYahoo, “those of whom we cannot speak”, “your friends whom we can’t talk about”, “a certain small ethnic group”, the chosen, the tribe, the chosen tribe, the thirteenth tribe, tribe of Judah, the Khazarians, Khazarian mafia, Rothschilds, Khazarian Rothschilds, JewTube, JooTube, JewMerica, JooMerica, etc., etc.); no being nasty to other commenters; no trolling the “sysop”; no passive-aggressive needling of the “sysop” (I don’t acknowledge, I just BLOCK and you’re gone, “one strike” and your ass is out, GO GET SOME THERAPY); no dissing or ragging on the Insane Clown Posse, no Chupacabras, no “country music”, no karens or avocado toast, no complaining that your other comment wasn’t published (because you’d didn’t read this Comments Policy), and no claiming “the korona doesn’t exist because vyruses don’t exist.” Please share your ***CONCISE*** (2 smartphone screens of small font text is NOT concise, I don’t have time to read your dumb fucking manifesto, gawd dayyuuum!!!), relevant, coherent, organized thoughts, and come back for my next post. Also, by commenting, you expressly accept and agree to my “one bullet, one Nazi” policy, and please be advised, this includes Nazis everywhere, even in the Ukraine. Furthermore, if you are a LibJew/DemJew, you are BANNED from commenting on this site UNLESS you acknowledge the extensive presence and influence of Nazis and other fascists in the Ukraine, who don’t give a fuck that they have an allegedly “Jewish president”, because they’re still (in many cases) getting paid by the state, and they’ll “take their country back from the Jews” once they take care of the Russians (can’t slit all throats at once.) If you can’t acknowledge it, then get the fuck out with your “Never Again” bullshit. Also, no scrubs. If you don’t know what a “scrub” is, please consult the TLC video on YouTube. Although scrubs exist in ALL ethnic groups and populations, a very good example of scrubs, is all the poor young black men who get shot dead, and then the moms are like, “He had such aspirations, he was going to be a rapper.” Yeah, they were all going to be famous rappers, all the thousands of them! Sure!

Seems to me so called investors are catching a lot of flack. I can’t tell you what that means but have heard it floated by Normies a couple of times. I assume that means stock/share holders? Here is a reddit headline that found its way thru my email.

“President Biden: “Investors in the banks will not be protected. They knowingly took a risk, and when the risk didn’t pay off, investors lose their money. That’s how capitalism works.””

Not going to click on it but it shows in the email 13k upvotes. It vexes me how easily some are led astray but it no longer surprises. If that is the case I have to think stock holders should be jumping out of any financial institution. Again, maybe it is something else they are referring to that I am overlooking. It’s probably the dopamine hit they are shoveling to the masses.

I can vouch for the bond examples given in this post. Many different people I have listened to over the last several months have made similar remarks.

Jacob are you still looking to do a logo change? I have something that fits nicely. I can’t design worth a shit but I am fantastic with slogans…..

“The Blog Nazi….He suffers for His Blog.”…..”NO BLOG for YOU!”

That thing about “investors in the banks won’t be protected” sounds like complete bullshit to me. What serious investors thinks that they should somehow be “protected” when they’re holding the bag on a long stock position that tanks?? Also, if SVB is “made whole” by the Fed, then it’s just a matter of time before SIVB turns around — if the story is true.

A big part of corporations is this ESG thing which is a complete farce and is strongly enforced by banks. They don’t want to provide loans to businesses that don’t toe the ESG line. The whole ESG is a stupid idea that doesn’t make fiscal sense. Organizations participating in it *should* have problems.

I have recent experience with bonds. I’m holding an FHLB bond with a 5% coupon rate but that’s an “agency” bond. Most corporate bonds are less competitive than brokered CDs lately. Treasuries have been consistently outperforming them. I picked up some 13-week T-Bills at auction just yesterday and it was 4.8% or something like that.

I also think the whole loudly heralded “this is the beginning of the banking system crash” is largely bullshit too. Sure, some are stretched thin and have made bad bets but I’ve yet to hear about any of their underlying investments actually defaulting. Interest rates moving against them combined with ESG lunacy should mean that some have serious issues or fail.

In today’s video, Jeff Snider goes into detail that this is a global liquidity crisis. The recent Federal Reserve action of keeping the discount window open for one year and preventing banks from selling their T-Bills is quite futile as the banking problem is that the depositors businesses are not generating sufficient money to cover their operating costs and forcing these depositors to draw down their cash from these banks. We are entering into deflationary world! Here’s his video and is quite educational: https://www.youtube.com/watch?v=bPlaLs-H_yc&ab_channel=EurodollarUniversity

You can find my same post at Eurodollar U. SVB had no risk manager for a long period, in fact turning over those reins after the departure of the previous manger to their diversity manager. Hence they did not hedge for changes in interest rates causing the 21 billion to be sort of “uncovered” and losing value which could have been protected by these hedges “against rising rates suddenly turning into falling rates”. This reminds me of the movie “Margin Call” where the analyst tells the CEO how underwater they are to the point of “insolvency” due to bad positions that weren’t hedged..

No offense, but no one cares where else you posted your comment, sorry. As to the rest of your comment, you’re still carrying the duration risk propaganda. The bank had a solid portfolio, oriented around longer-duration mortgage bonds. As to something about diversity, you’re just vaguely carrying some stupid conservative “talking points” that you read somewhere. Given their size, of course they had plenty of risk management analysts. SVB may have been a woke organization, but there’s nothing they could have done; EVERY U.S. bank with an overweight bond portfolio is likewise insolvent if rates go back to what they were mid last week. SVB was simply honest about its bond losses, announced it (by updating its income statement with an impairment), and everything went downhill fast, from there. You have ignored literally everything I wrote on this topic. Maybe try listening, for a change?

Are you actually going to use your Locals.com site? Not being pushy, just curious.

DiMartino in this interview goes beyond this aspect of the economic crisis. She makes the point that things have been falling apart for quite some time. For example, she points out the crappy situation with the car industry – no one is even showing awareness. She gets it that the propaganda machine is distorting our perception of reality.

https://www.youtube.com/watch?v=vijw7dKHYHg

BTW – will there be coffee mugs for sale with the new logo mentioned by luke?

The question is – does the Fed want small retail banks to succeed or are we centralizing in the same way that lockdowns shut down small businesses but left the big ones open? Some banks are “systemically important” while others are not. Maybe they don’t even want the small guys to fail, but some may be sacrificed to save the international status of the dollar. No matter which way it is intended, we are in a financial end game for the current financial system. Likely they do not have any real plan and they are just reacting now. Cash in your wallet instead of the bank is in the air.

Reposting my reply from the last blog re this…

“It does, and thats why they need to flip the tables( ;D ) at the systemically insignificant banks, so they can be bought out by the systemically important banks, WHICH LITERALLY OWN THE FED, and then CBDCs no longer hurt the commercial banks left. The CBDC’s will be owned and controlled by those commercial banks and their already wealthy investors( see oligarchs ).”

I have just dusted down my treasured copy of ‘Stabilizing an unstable economy’ and am rereading. If this is not the ‘Minsky moment’ it cannot be far off. The only problem is that I have been saying this for the last ten years or more and some how the rascals manage to wriggle out of it and borrow a bit more.

This must be pretty frustrating for V.Putin too, with his immaculate debt free, balanced budget economy. “When are these damned Yankee imperialists going to run out of other people”s money and go home and leave me in peace to rebuild my country?” he is no doubt muttering to himself.

Ordinarily, nobody would say that holding AAA rated government bonds is risky!

The drivers of this seem fundamentally similar to the pensions problem the UK had in the autumn. Funds held government bonds, whose values fell as interest rates rose. The funds had borrowed money to hold the bonds and their main assets were illiquid (PE investments and so forth) so they did not have the cash to meet collateral requirements when the bond values fell. For a bank, the equivalent liquidity challenge is being able to pay its depositors on demand.

We will no doubt see more drama as interest rates change.

That’s the problem. “Holding gov’t bonds” means that you are lending money to the US Federal government.

How have they used that money over the past 40-50 years? Any new shiny assets that are generating large income streams? If not, then you just lent money to an entity that wasted your wealth. How does that not carry repercussions at some point?

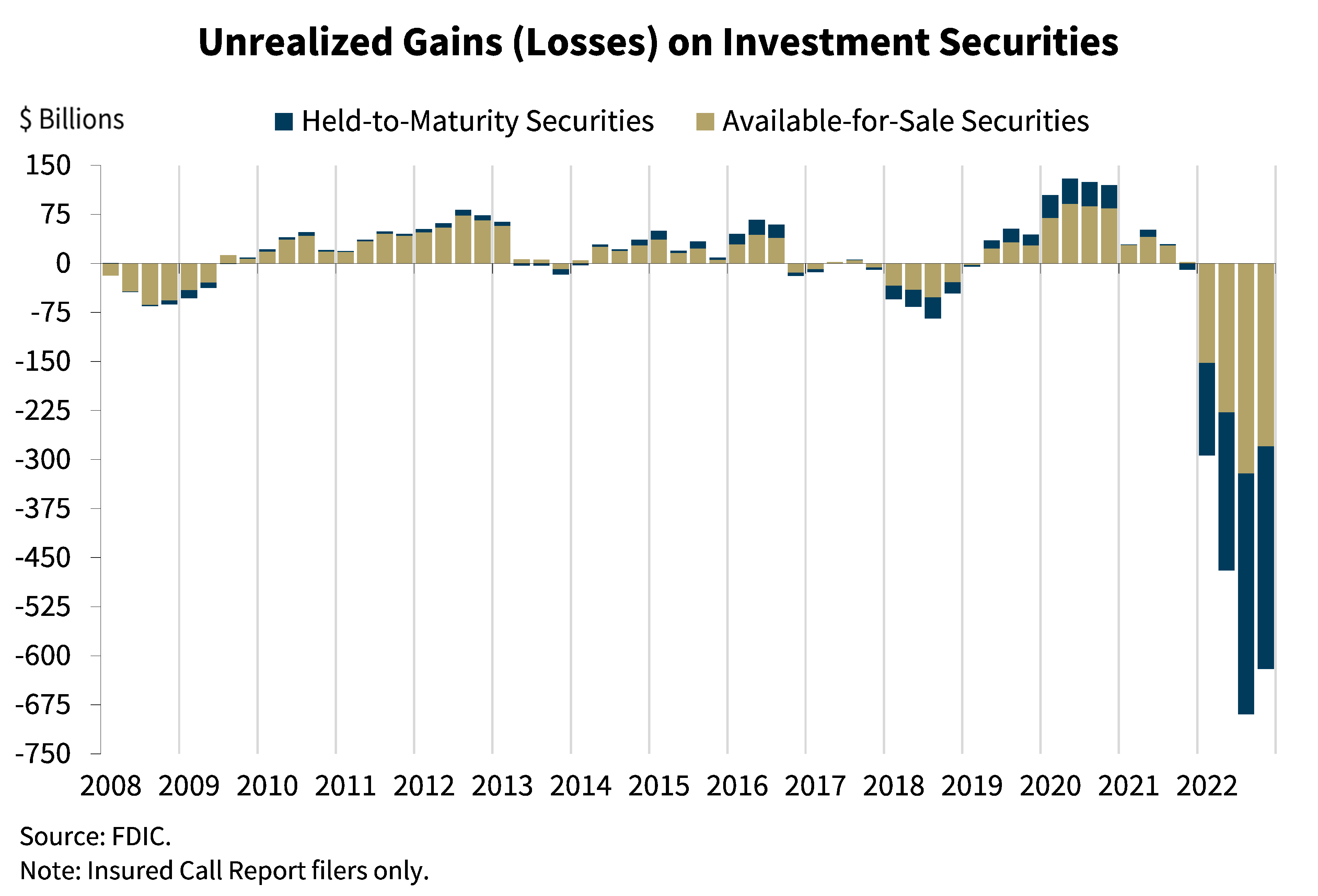

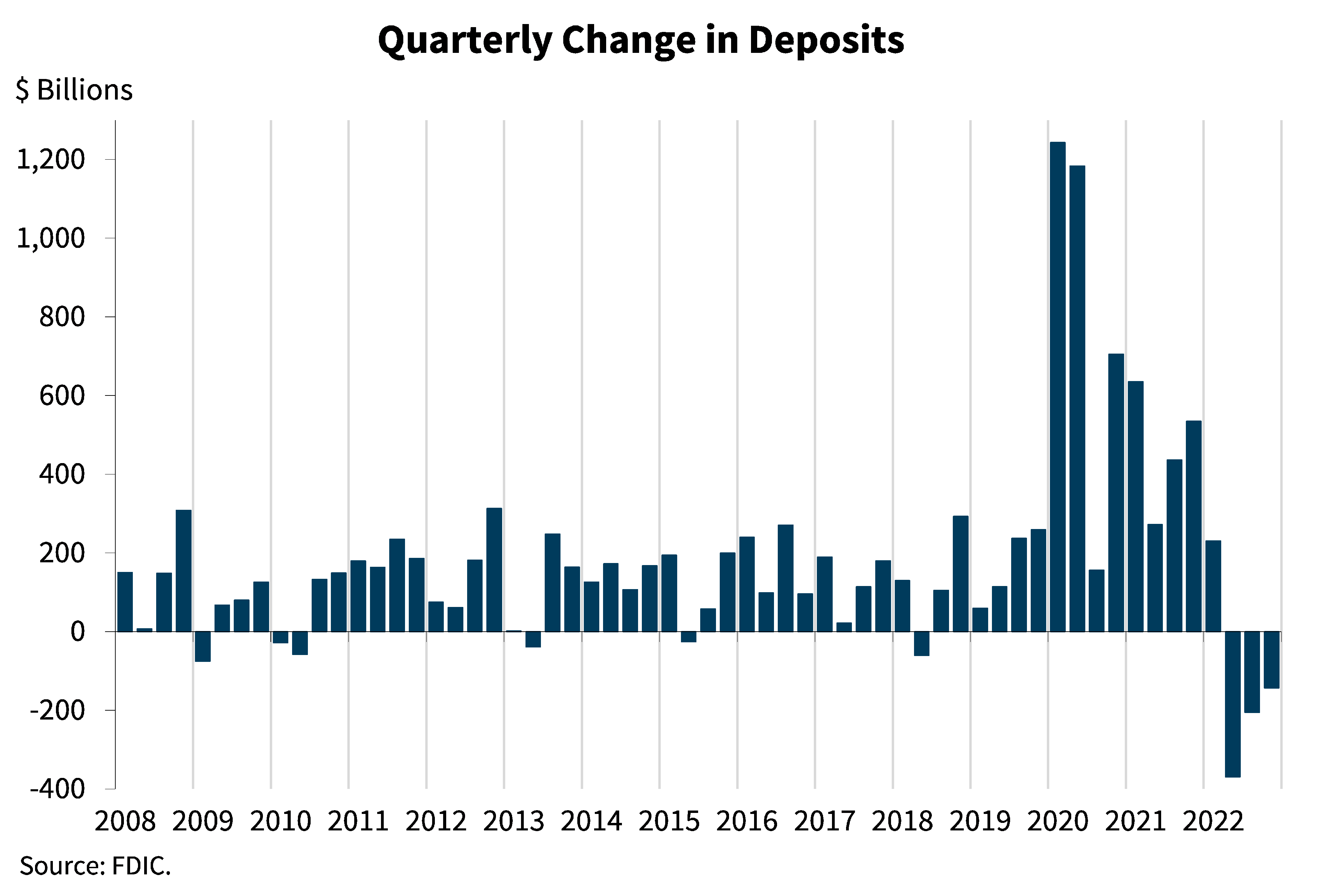

FDIC reported significant aggregate unrealized losses in member banks during 2022.

And contemporaneous reductions in bank deposits.

I wonder how many banks are insolvent right now. Full comments:

https://www.fdic.gov/news/speeches/2023/spfeb2823.html

Are we going to se QE again?

Question: in your opinion, are the rising interest rates motivated by a desire to ‘fight inflation’ or by a need to defend the value of the dollar internationally? In a thoroughly ‘financialized’ economy, a lot of the price increases are due to the interest rate increase. What kind of sense does it make to bail out banks that are failing only because of central bank policies aimed at reducing inflation?

Price increases are not due to higher rates, LOL. They are due to the volume of goods and services on offer, not growing commensurately with the explosion of the money supply in 2020-2021.

As to your good question, it’s all about inflation.

I’d write much more, but, my lunch break will end soon.

Thanks for your comment, all the best to you.

So the Fed can’t raise rates at all without triggering another housing and banking crash? What happened to all those “stress tests” they instituted after 2008?

And does anyone know (approximately) how big the SVB assets minus liabilities number is? Billions, 10s of billions? I have trawled through a few WSJ and FT articles but they don’t give any idea of the scale.

I read SVB was about $15 billion in the hole.

My recall might be off here, but didn’t the FED waive bank reserve requirements on treasuries in order to entice banks to buy treasuries?

They were incompetent. They got upside down by being too long. The longer the date, the more it falls. Other banks did the same and they have been bailed out now. The bigger banks can’t get that upside down without people noticing. The shorts saw the imbalance and they took them out and the run started.

Inflation will stay higher but the fun is over. Too many losses taking place and more to come. Private equity about to take it on the chin now. That is the biggie. So we accept a higher rate of inflation in the future and capitalism gradually collapses as we enter into zero growth. A world turned upside down.

Salute the flag, God Bless America and long live Ukraine!!!

Sorry, you’re wrong, you haven’t paid attention to my long headline, you’re carrying the propaganda “talking points” nonsense about “duration risk.” Only you’ve got it confused, you’ve got it from the side of “they were too long”, when the propaganda is “too short.”

In reality, 2yr and 10yr yields went up together, same trajectory, same timing, and were, at the peak, just 1.00 apart. The SBV duration risk story is BS. All banks are potentially at risk.

I’d write in more detail, but, gotta go.

No, there are plenty of problems. Everything is fake it until you make it at this point. There is not enough growth to carry on the capitalist model. It is never ending bailouts to try to keep the system afloat before it collapses. This is the beginning of the end. They are stealing everything that is not nailed down. The dawn of the new era. An era no one want to enter into — left, right or indifferent. Just let it last a little longer.

It’s low growth and fake accounting from now on.

Even if the yield on the 2 Year and the 10 Year were identical (and moved up and down in tandem), there’s more interest rate risk on the 10 year, since it has to be discounted to a greater degree after rates have risen to compete with newer, higher rate-yielding securities. Consider a one month T-Bill vs a 30 Year bond. The bill has no rate risk, the bond has huge rate risk, and it has almost nothing to do with their relative yields at any point in time.

Mortgage-backed securities are always hard to value because the duration is less knowable. When rates fall, average duration shortens as people refinance. When rates rise average duration lengthens as people stay in their houses longer than was previously expected. Yields on MBS’s are higher than on 10 Year Treasuries to compensate for the unknowable duration. SVB was reportedly heavy into MBS’s. Duration was what killed their assets while focusing on tech startups put them at risk of deposits being yanked. They failed Banking 101. Actually, I think they skipped that class entirely and took Intersectional Feminism and Gender Affirmation.

Your overall point is spot-on: ALL banks holding much in fixed assets: Treasuries, MBS’s – even portfolio fixed rate mortgages that they own and service – are upside-down on those assets, and a run on deposits will prove them insolvent – unless the Fed cuts rates quickly (ensuring inflation as far as the eye can see).

<<.....there’s more interest rate risk on the 10 year, since it has to be discounted to a greater degree after rates have risen to compete with newer, higher rate-yielding securities.>>

Thanks, great comment overall, but I think you’re looking at this the wrong way. With an INVERTED yield curve, they must have lost the most money on their shortest duration bonds (e.g., 2 years outstanding) and bills. It’s not the 10-years that were the problem, Wouldn’t you agree? Of course, again, all banks would have this same problem. The short stuff was only a relatively small part of SVB’s portfolio, the bank did nothing wrong with its “duration” management overall.

I can’t speak much to the MBS in SVB’s portfolio, other than, looking at the FFIEC Form 31, it is overwhelmingly 15+ years… and, that 15+ MBS is by far and away, the largest component of the entire portfolio. In fact (just going by memory), they have about as much 15+ MBS, as they do Treasuries of any duration. Which obviously puts to rest the talking points about “they were too short duration in their portfolio.”

All the best to you.

Sentient is correct. In an environment where interest rates are continuing to increase, there is a risk of having to give ever greater discounts on longer term bills the longer they’re held. The higher the rate goes, the greater the discount that has to be given by the seller if they need to cash in on bonds they’re holding that they previously bought at lower interest rates. So if interest rates continue to increase over time, the discount the seller potentially has to give on bonds they’re holding long-term continues to go up, and the greater the sellers capital loss.

This only stops if interest rates stop increasing, which, as you say, is likely now.

Anybody catch the last television commercial SVB had aired prior to their collapse? Its out there….check it out. My goodness they were proud of only one thing……their pandering to wokeness. One has to wonder if Joe, when proudly announcing the firing of management at SVB was aware that the President of the bank was a “Latinx” lesbian? That is about the extent of the womans resume which as one can now tell, is not surprising.

What about rumors of insider trading (selling) just week before the crash?

Hello. There’s no rumors and nothing insider. It’s simply a misunderstansing on the part of those reading certain news. There has been much news on who got their money out, and when. Some earlier, others later. It was a deposit run. Many are reading into it, what’s not there.

Do you think this will affect the US financing of Ukraine? It is indeed hard to imagine that Biden or Yellen would come out and announce another $5B to Ukraine…

It means that they’ll send “$5B to Ukraine” that will be as effective as “$4B to Ukraine” last month or “$3B to Ukraine” two months ago. Welcome to hyperinflation which is just another word for lowered living standards.

Don’t know about “duration risk”. The term is duration mismatch. They locked in on long dated paper. Let’s say they locked in at 2% for 10 years using a treasury bond, assume at a cost of $1000 ea.. They pay 0.1% interest to depositors. Those accounts are essentially zero duration. Interest rates (Fed Funds) rise to 4%. Depositors want a higher rate as they can get 4% on T-bills. So they start withdrawing. The Ten year bonds SVB bought 2 years ago are now around $700 ea.. They HAVE to sell these bonds to get the money for depositors. 30% loss. They can use the Fed discount window, but that’s going to be 4.5% interest. But they are only making 2% on their assets.

They should have hedged, but they didn’t.

Some serious misunderstanding here. The yield is never locked in, only the coupon is locked in. And you can sell your Treasuries any time, perhaps at a loss, but it’s not like a $100 paper bond certificate that you buy for your nephew as a novelty, and he holds it until it matures. In the adult world of AAA bonds, no one is “locked in.”

The REAL “duration mismatch” is in a bank’s non-callable loan portfolio, but in that case, ALL banks, EVERYWHERE, have duration mismatch, ALL the time, since the DAWN OF BANKING.

Pretending (as “they” have done) that this was an SVB problem only, to deflect from the systemic crisis, is REALLY dishonest. As if all these smart people, don’t know what banking is about? Yeah, OK.

They were just seeding talking points among the peasants. I saw it play out in real time with Bill Ackman being carried by “Citizen Free Press”, which is a sort of reboot of the Drudge Report, very popular.

A LOT of proles have fallen for it, more than a few commenters on this site have fallen for it. So many of them repeating the “should have hedged” BS, like they are experts all of a sudden. Do they even know what “hedging” is?

The only hedge is for the government to maintain an atmosphere of confidence, all the time. Any bank will fall if enough depositors start asking for their money, and don’t stop. You can’t “hedge” against that.

This reminds me of July 2014, when the Malaysian Boeing was shot down over Donetsk, and everyone became an overnight expert on the alleged trail of “the Buk”, and the rebel personalities allegedly involved, some guy code-named “Beast” among others, LOL. That guy was probably too busy raiding police stations for bullets. He was in charge of the Buk, like I’m a pimp in a fur coat. It was all BS.

But people are all the same, always. If one doesn’t understand something, it’s a new or unfamiliar topic, one will latch on to whatever talking points are going around. Critical thinking is always in very short supply.

We are all, always, at risk of being a sock puppet for some spin-master. Some much more, some less, but there’s always some risk.

“A LOT of proles have fallen for it… So many of them repeating the “should have hedged””

Clearly, many have no idea of what hedging is about and how it is done. Forget about all the specific ins-and-outs of hedging. The question is, “Who or what institution is big enough, willing and able to be on the opposite side of such theoretical hedges for all the banks in the USA, much less the world?” It certainly isn’t Goldman Sachs, J.P. Morgan or the various exchanges handling such trades.

Bingo.

Hudson: “So far, the stock market has resisted following the plunge in bond prices. My guess is that we will now see the Great Unwinding of the great Fictitious Capital boom of 2008-2015. So the chickens are coming hope to roost – with the “chicken” being, perhaps, the elephantine overhang of derivatives fueled by the post-2008 loosening of financial regulation and risk analysis.”

The US banking system is a morbidly obese man on a couch being told to get up and run a 5K (much less a marathon). No wonder Brandon Fraser just won Best Actor.