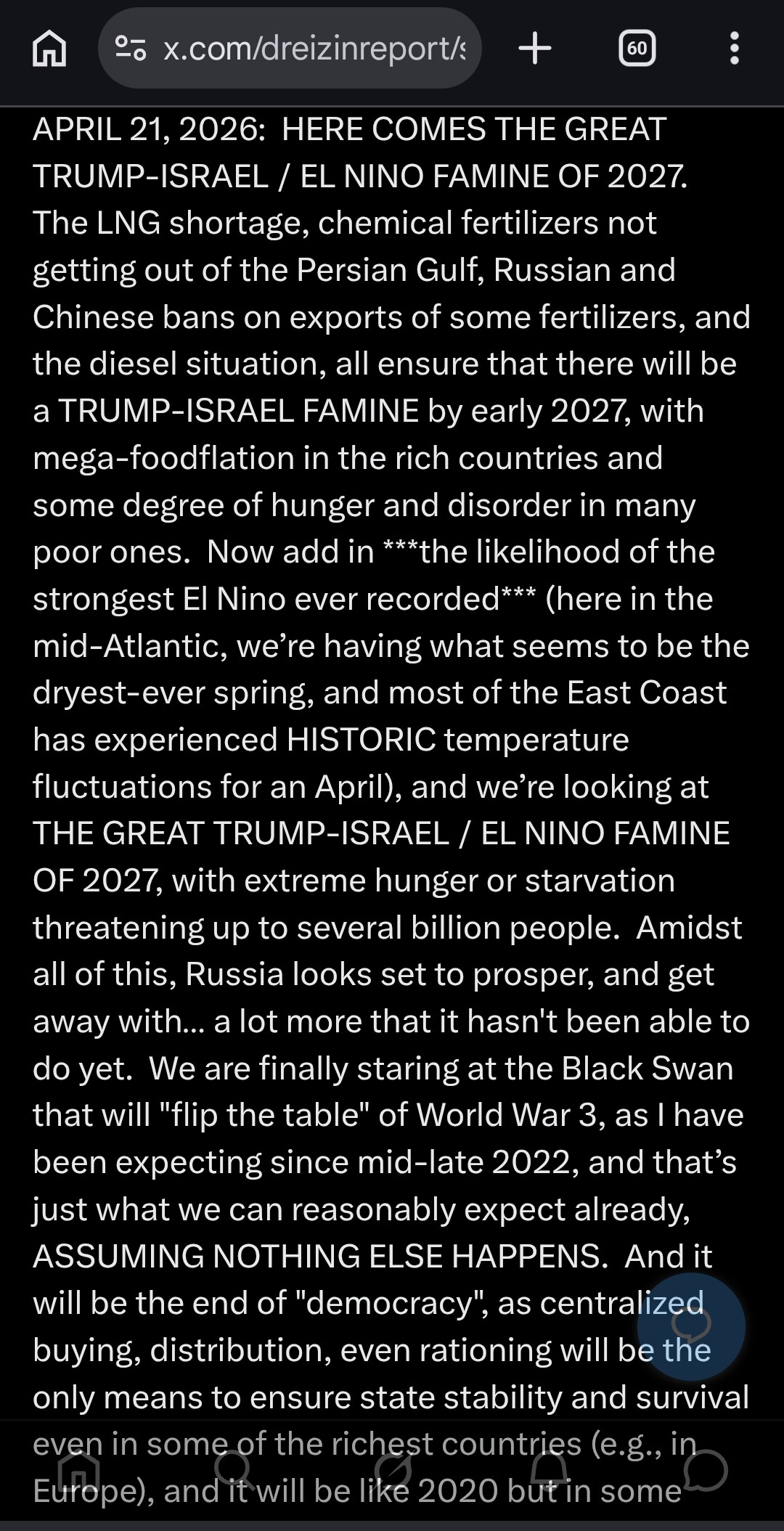

2022 is shaping up to be the first-ever “global” famine year, and that won’t bode well for prices in our supermarkets. Let’s take it one step at a time and see how we got here, also with an eye to what Republicans can do or say about it.

Global energy shortage

- The wind turbines that normally power one-third of Germany, also much of the Netherlands, UK, and other European countries, have been (and still are) unusually still this year, reportedly producing as little as one-fifth of what was needed/expected. There just hasn’t been much wind. Europe has had to compensate (and is still compensating) by burning much more natural gas to generate power. Renewable energy is great when it works, but it doesn’t always work.

- Hydropower in Brazil and the Andean countries, also most countries in Central Asia, as well as our neighbor Mexico, is doing very poorly. Drought conditions in many regions have led to reduced water levels and thus reduced flow through the turbine sluices. Brazil has had to import much more U.S. liquified natural gas (LNG) for its power needs; other countries are burning more coal (or going dark) to compensate.

- In other news, over the last few years, “activist” hedge fund managers have gotten on the boards of the largest Western energy companies, shaming/intimidating them away from new investments in oil or gas extraction, in favor of “green” investments (which may or may not be actually profitable.) Western sanctions on Russia and Iran, as well as the Israel-Lebanon maritime dispute, have also limited exploration and shut down or severely restricted potential new mega-projects.

- It’s gotten so bad that, in real (inflation-adjusted) dollars, investments by U.S. and European companies in new oil or gas projects are at or near multi-decade lows. The Brandon Administration’s crackdown on pipelines and on drilling on Federal lands has exacerbated this problem. No one wants to put up big investments now, when regulatory and PR knives on both sides of the Atlantic are out for the fossil fuels industry. It’s easier for the oil and gas firms to simply “wait it out” while sitting on record profits from higher prices. (Of course, they will be demonized either way.)

- Keep in mind, nothing “green” can heat your home in winter. You have to burn some flavor of natural gas or (in many countries, for home stoves or for district heating) coal. The Green Religion has no solution for this. The Greens want to crack down on fossil fuels so that electric generation shifts to renewables, but they have no way to keep you from becoming a corpse-icle in wintertime. They also forget that natural gas is essential for chemical fertilizer production, to keep humanity fed (more on this below.)

- There is a global bidding war on for coal and LNG. With respect to LNG, Europe is competing with East Asia (mostly Japan and Korea) is competing with Brazil. East Asia traditionally pays much more. Europe is losing out, and you can imagine it is hard for a country like Brazil to stay in this game. Then there is Ukraine, which is running out of both coal and gas, forcing it to go full steam on its Soviet-era nuclear reactors, to include cancelling scheduled or ongoing maintenance on a number of units—certainly, there’s nothing to worry about!

- China has hit “peak coal” over the last two years; its huge domestic production is on an as-yet shallow but irreversible downslope. So, all coal importers must now compete even more strenuously with China on the global market. Note that China still derives 70 percent of its power from coal—it is far behind almost all other industrialized countries in its diversification. China’s nuclear power, as a proportion of electric generation, is barely even on the map. China recently made a show of planning for scores of new reactors, but that is ten-plus years away. This country will be gobbling up an ever-greater share of global coal indefinitely, keeping prices high. The era of cheap thermal coal is over.

- There are reports of diesel shortages as Chinese trucking competes with Chinese manufacturers burning diesel for their backup generators when the power goes off, as it has been doing. This may get much worse before it gets better. As of now, our “supply chain” horror story is about longshoremen, truckers, and warehouse workers here in the U.S., but soon enough it could be about Chinese suppliers no longer being reliable due to their own problems. We could fix everything here and still have big shortages in 2022.

Global fertilizer shortage

- The problem with burning more natural gas is that you have less of it available for fertilizer production.

- Most chemical fertilizers rely on natural gas as a “feedstock” or key ingredient in the production process. Through a series of reactions, hydrogen in the methane gas (CH4) is transferred to form ammonia (NH3.) Nitrogen in the ammonia is essential for chlorophyll and amino acid synthesis inside all plants. Although our atmosphere is mostly nitrogen, plants cannot use free nitrogen. Nature has ways to get nitrogen into the soil as ammonia, but it’s not enough. Chemical fertilizers solve this problem, and have supported massive increases in crop yields (and thus, population) in the last century. Without chemical fertilizers, most of us would starve to death.

- When renewables such as “wind” or “hydro” fail, you have to burn more gas for power, and again, the problem with burning more gas is that—if you do it in “unplanned” fashion, without raising production, finding reliable new import channels, or keeping more in storage—you have less of it left for fertilizer production. Even if you are compensating by burning coal not gas, you are “snatching” that coal away from someone else who might have to burn gas. We cannot get around this problem. Even “just” a coal shortage, means a fertilizer shortage.

- A number of fertilizer plants in Europe have slowed or simply shut down (taken a production pause) due to the gas shortage over there. Presumably, Europe will have enough (more or less) fertilizer for its own needs next year, but it won’t be exporting nearly as much of it to developing countries.

- Reportedly, Russia has instituted some type of export controls on chemical fertilizers, to ensure that it has enough for itself first and foremost. I’m not sure if the U.S. has been impacted by this yet, but generally, about 40 percent of ammonium nitrate and 20 percent of urea used in U.S. agriculture is imported from Russia.

- CF Industries Holdings, Inc., the U.S.-based fertilizer giant, put out a red alert on a recent earnings call, stating that (as summarized by Bloomberg) “farmers won’t be able to get what they need.” As CF Industries produces and sells in a number of countries, it was likely not speaking about American farmers specifically. However, prices for “basic materials” tend to be—if not global—then at least, globally influenced. Ultimately, everyone is competing with everyone else for everything.

Global food shortage

- Russia’s share of Latin American fertilizer imports is even higher than it is here. Latin America is a weak domino. If Russia can get a better price from China, then “south of the border” may have a very poor harvest. And if they can’t eat, they will be coming here, in numbers as yet unseen. You think you’ve seen a big “caravan” from little Honduras? Wait until Mexico comes over for dinner.

- Many countries in the Muslim world—Egypt, Syria, Lebanon, Iran, Afghanistan, among others—are already just barely surviving, and much higher costs for imported fertilizer and food can push them over the edge very quickly. We saw this with the “Arab Spring” in 2010 and 2011, but it’s looking to be potentially worse now. That’s surely wonderful news for Europe and its migrant situation.

- The U.S. will be affected. Even if we have enough fertilizer here, every nation’s agriculture is influenced by global prices and demand. This has been clearly demonstrated in Russia, the world’s largest wheat exporter, which has had to curb exports somewhat, to keep bread and noodle prices from blowing up at its own shops and bakeries. Simply put, if your middlemen can get a better price elsewhere, the product will start leaving your borders at a higher than usual volume, and export controls become necessary—although the U.S. even talking about capping its grain exports would likely spike prices worldwide.

· The grocery price hikes that we’ve seen so far in the USA, are just the start of a trend.

They are not “transitory.” We can expect huge inflation and “shrinkflation” through all of 2022 and into 2023. Of course, prices of other goods and services will boom as well, which is “great news”, if you believe Brandon’s spokeswomen and the Democrat media complex. (Soon enough, it won’t be “great”—it will just be “Trump’s fault.”) But that’s beyond the scope of this fact-sheet.

Political aspects

- Republican talking points will probably go like this:

- “We need power from all sources. Renewables can be great, but you can’t crack down on oil and gas and expect food prices not to go up. You need natural gas to make fertilizer, you can’t get around it. If there’s not enough natural gas, people will go hungry. What the Left has done is try to socially engineer a Green Revolution, forgetting that we still need fossil fuels to make food. They tried to solve one problem, but they created others. And now, people can’t eat, and governments are falling. We don’t need Ideological Leadership—we need affordable energy, and food on the table.”

- “Grand Moff Tarkin” a.k.a. Merrick Garland can keep signing

ORDERS TO DESTROY REBEL PLANETSpolitical search/arrest warrants on the deck of the Titanic—it won’t make any difference to the ship. There will be nothing left of this would-be dictatorship, soon enough. They are a nasty runt dog pissing on your beach towel, with the water receding and a tsunami approaching. The day-to-day noise is the runt, the big picture is the wave. - Republicans should just be right and sit tight. Try to help the politically persecuted, build your organizations, true the vote, don’t pull a Todd Akin. Give to your local food bank. Better yet, build “prophet credibility” by getting your candidate or local party brand involved in helping your food bank BEFORE the wave hits. Food, inflation, and shortages will define 2022 and much of 2023.

Afterword

- Barring any major catastrophe that begs comment, this will be the last edition of the Dreizin Report for 2021. I look forward to communicating in the New Year. If you did not receive this fact-sheet directly from me, please email jacob@dreizinreport.com to get on my mailing list. Thank you!

UPDATE : December 3, 2021

I wasn’t going to write any more this year, but things have gotten much worse since below. Word is that congressional Republicans have resolved not to have any agenda for the midterms, and when you consider how fast things are going downhill, it’s just as well—anything they come up with now, will be irrelevant well before November 2022. Of course, they are thinking about inflation generally.

My specific focus is on food prices and food shortages. Price charts for all types of agricultural fertilizer sold in the USA are still on a vertical up-slope, well past their previous all-time highs. As of now, predictions of doom and distress from fertilizer supply guys are being carried in farm publications here in the USA and in Canada.

It is now clear that there will not be enough fertilizer available for 2022 spring planting not only in developing countries such as India, but also here at home.

The Federal bureaucracy is only making things worse, in a form of national and global assisted suicide. On behalf of CF Industries Holdings, Inc., they have levied or are about to levy anti-dumping penalties on nitrogen-based fertilizer exporters in Russia, Morocco, and Trinidad. Russian exporters, in particular, who reportedly provide about 40 percent of our ammonium nitrate, may be required to put up a cash deposit of around nine percent on their shipments here.

This is great for CF’s bottom line, not so great for farmers and the rest of us. It is clear that the administrative machine is (as always) totally clueless and lacking in any big picture vision or coherence. Worse still, Uncle Sam has just sanctioned the main export arm of Belaruskali, the Belarussian enterprise that accounts for one-sixth to one-fifth of global potash trade. Although the U.S. likely gets no potash directly from Belarus, this may push up potash costs for everyone by possibly forcing the state-owned firm to avoid all dollar-denominated transactions.

On top of that, “global warming” is on hold as low temperature records get blown out almost every day throughout Europe (among other places), forcing the continent to burn more natural gas for heat, leaving less and less available for fertilizer production. In fact, Europe’s fertilizer picture is so bad that they are now (in preparation for the next growing season) importing the stuff from Egypt. Meanwhile, they are shaking the toy sword more frantically than usual at Russia, their main gas supplier. Oh, and China has curtailed its own fertilizer exports, half of which go to India.

Everyone who can get away with it politically, is putting up barriers on the way out or the way in. We are sleepwalking into a planet-wide food crisis that will deliver nationally and globally unprecedented price hikes and shortages just in time for… the midterms. Everyone who enjoyed last year’s BLM/Antifa looting and arson, should buy some popcorn for the upcoming My Kids’ Tummies Matter edition. “Loss prevention” at supermarkets will certainly be the new growth industry.

Worst case, of course, we can eat the Karen’s. Please do keep in mind that, just like Trump personally killed every single Chinavirus victim on his watch, this will all be Brandon’s fault.

2nd UPDATE : December 15, 2021

The European energy picture is degrading at an accelerating rate. From Finland to France and almost all points in between, wind power generation is still (same as all year) off by about one-third relative to what is “normally” expected. For countries like Germany and Denmark that rely on wind for about a quarter (or in Denmark’s case, closer to 40 percent) of their electrical generation, this is a massive hit that requires burning more coal and natural gas to compensate—but the gas is just not quite there. Or rather, it soon won’t be.

The great system of underground gas reservoirs that was set up with Gazprom’s help about 10-11 years ago, has gone from 68 percent to 60 percent full (the latter figure being more consistent with mid-January in a normal year) in just the first two weeks of December, before winter has even properly started in most European countries. And in the Ukraine, the winter gas storage top-up has been used up completely—they are back to where they were around late October.

The one thing keeping Ukraine from melting down now is power imports from neighboring Belarus, which can be shut down in a blink if Russia wants to really turn the screws. Keep in mind, it is likely that this winter will be much harsher than usual in Europe—north Scandinavian temperatures have reached or blown out record lows, and parts of Scotland and north England have seen once-in-a-generation freezes and snowstorms.

It seems that “global warming” is taking a break, and that scientists who ignore “the agenda” and instead link reduced sunspot activity to falling temperatures, may be right in their “little ice age” predictions. Despite all of this, European “leaders”—more Three Stooges than Congress of Vienna types—are still preoccupied with vaccine passport nonsense, and the Germans are still playing high-stakes chicken by slow-rolling (or no-rolling) certification of the completed Nord Stream 2 gas pipeline from Russia. In exchange, Russia is fulfilling all its gas contracts but offering few if any new contracts on the spot market.

Electric prices have responded and are now spiking—the day-ahead wholesale price of a megawatt-hour in the Baltic countries (Europe’s weakest and most useless domino) has reportedly reached as high as $1000 in intraday trading, many times above normal. At this price, if states run out of funds to subsidize household usage, then the lights will go off very quickly. At the same time, fertilizer prices continue to spike; anhydrous ammonia in the U.S. now costs an estimated/surveyed (there is no firm benchmark) $1300-plus per ton, up 18 percent from early November, according to one guy who researches this stuff for the authoritative Progressive Farmer website.

And after Uncle Sam piled on to the European Union sanctions against Belaruskali—which produces 16 percent of the world’s potash—the usual Lithuanian export route for this Belarussian product is expected to close potentially within weeks, as the Lithuanians are very keen to make America happy. The stuff will now have to roll the long way around the Baltic countries to Russian ports near St. Petersburg, probably adding ten-plus percent to the sales price.

Furthermore, as far as I can tell from the news, Washington is still on track to implement penalty tariffs on foreign fertilizers at the request of market oligopolists CF Industries and Mosaic—total insanity at a time like this. The price situation is so bad that a farm group has asked Merrick Garland to launch an investigation, but what is he supposed to do, investigate his fellow cabinet members? Lastly, the fertilizer supply situation in India is looking desperate, there is a natural gas shortage in Pakistan (due to cold weather on the periphery), and China has continued a ban on its phosphate exports, keeping about a quarter of global cross-border sales volume off the market indefinitely. At this point, I should disclose—to keep Brandon’s SEC and Garland off my back—that I am personally invested in the price of fertilizer going way up, although I am not recommending any particular method to bet on that, and in fact, I insist that you don’t try it yourself. I am not selling anything.

The world continues to sleepwalk into a famine situation as of late 2022.

(If this is your first time seeing this email chain, please read below to understand the connection between natural gas and nitrogen-based fertilizer.)

I’m not sure how it will play out here, other than I expect $5 loaves of Wonder Bread, and a lot of shoplifting, at a minimum. To say that Brandon’s party will be punished by a “wave” election is a gross understatement—it won’t be a wave, it will be more like a giant asteroid knocking half the ocean and half the atmosphere into outer space.

Reading this article this May 27 2022, I believe you should re-publish it as the relation between natural gas production and fertilizer production sheds new pertinent light on the present situation.

Impressive piece, thanks. I only would like to know more about the fact that Bill Gates has bought so much farmland apparently intent on taking it out of production. Is this decrease in farmland worldwide? And not only is the availability of fertilizer at stake, its use is taboo as well in India, Sri Lanka, The Netherlands, Canada, the UK and probably elsewhere.